The next series of posts will focus on certain aspects of real estate as it applies to members of the military. These posts are originally published on Trophy Point Real Estate Group’s blog and are written by a former Army Officer and current real estate investor, Pat Wilver. Today’s post will take a look at the decision to rent or own while the next few posts will give insight into your first home purchases and how to analyze an investment property. You may notice a Savannah, GA slant so those of you headed that way take note!

I tend to write too much in these blogs, so I’ll cut to the chase: The average homeowner who buys a starter home in the Savannah area will be $80,000 richer after eight years of home ownership than the average renter living in the exact same house.

Seem too good to be true? I don’t blame you — click here to see the math!

There are very few circumstances where it’s better to rent real estate than own it. They are:

- houses in the neighborhood you want to live in cost more than 200 times more than the average monthly rent in that same neighborhood (for example, if you could rent a house for $1300, but it costs $260,000 to buy, you may be better off renting that house, or looking for a cheaper neighborhood.)

- you expect that you will have to sell within two years (even then, it’s usually 50/50 whether it will be better to rent or own)

- you don’t have the ability to set aside a bit of money in case a large repair needs to be made

In my opinion, the chart below says it all. The middle column shows the median net worth of Amercans in a certain age group. The column on the right shows the same median net worth, but excluding home equity. The median American of retirement age is worth $223 thousand — and almost $140 thousand of that is home equity. If you aren’t a homeowner, you’re missing out on the single biggest driver of wealth in America today.

Factors to consider in the rent vs own equation:

Deciding whether it’s better to rent or own is part emotional and part hard numbers. I can’t help you with the emotional aspect, but I can help you look at the numbers. First we’ll have to collect some data. We need to know:

- Where you want to live, how big a house you need, and how nice of a house you want. This will help you determine how much it would cost to rent or buy a house that will fit your wants/needs.

- What kind of financing you can qualify for. We must determine your down payment and interest rate, and whether you will have to pay any mortgage insurance. (with the VA loan this is an easy determination!)

- How long you plan to live in the house, and whether you plan to sell when you move or place the house up for rent.

- Local data, including average appreciation per year, property taxes, insurance rates, and maintenance expenses that you can expect.

The Math

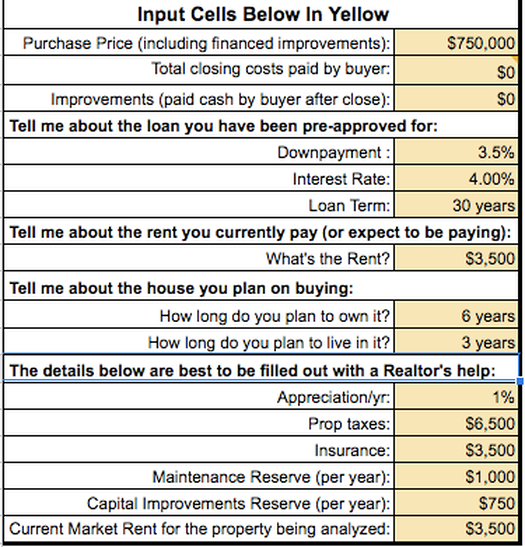

Let’s look at two example rent vs own calculations. In the first case, our prospective buyer wants to live in the heart of downtown Savannah. He’ll need a three bedroom townhouse. He’s got decent credit and will be using a FHA loan, which means he will make a down payment of 3.5%. The place is gorgeous and won’t require any repairs, and our buyer plans on asking for all his closing costs to be paid by the seller. He plans to live in Savannah for three years, and will probably sell after six. Let’s check out some screenshots from the Microsoft excel spreadsheet I use to run my rent vs own calculations to see if our friend should rent or buy.

The results: This one is a mixed bag. While it’s true that our friend would be better off in the long run if he buys, he will have to spend a lot of extra money for the six years he owns the house before he can realize that hundred and twenty thousand dollar profit he’ll make when he sells.

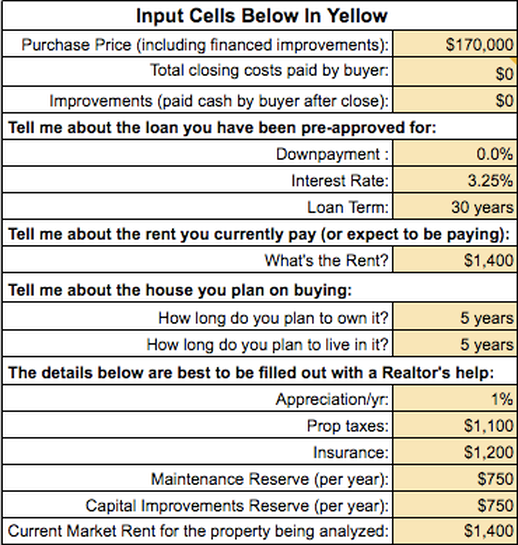

Next let’s look at a more typical case study. Our buyer wants to buy a simple three bedroom home out in Georgetown (a neighborhood in the Savannah suburbs for you out of towners.) She’s active duty military, so she’ll be using her VA loan and not making a down payment. She’ll probably sell when she moves away from the area, which she thinks will be in five years. Let’s run the numbers to see if our friend should rent or buy:

This case is pretty much a slam dunk — our friend should definitely buy instead of renting. She’ll be $42,000 richer at the end of five years if she buys instead of renting. It sounds too good to be true, but it’s not!

What Should you Do?

Pat has an awesome calculator to determine whether you should rent or own on his site here! But for those of you not headed to Savannah, Georgia, there’s another good calculator located here you might want to look at! $

Enjoy the content of this post? Subscribe below to get the latest delivered to your inbox!

Really useful tips here! Thanks for sharing this! I usually stay at hotels in Savannah GA during my business trips there and now houses for rent are a good option now! I better visit https://www.visitsavannah.com/vacation-rentals to check on which ones are the best since I’ll be staying over there a little longer this time!

LikeLike