Tired of paying rent? Don’t have enough money to make a down payment? Still want to buy a house?

The VA loan gives you the opportunity to purchase a property with a loan of up to $484,350 or more if you live in certain localities without requiring a down payment. The loan is eligible to individuals who served 181 days during peace time or are currently serving on active duty. To check your eligibility click HERE as you do need a certificate of eligibility. This post will discuss the process of how to use your VA Loan. Next time, we’ll talk benefits and why it’s worth it.

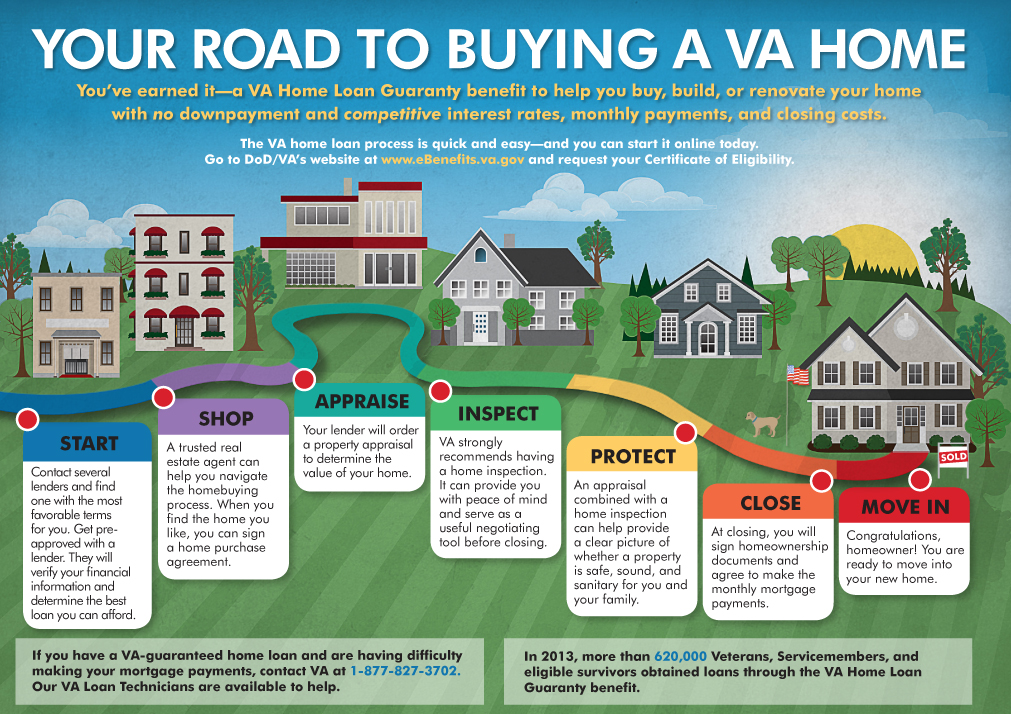

First, you have to choose a home you’d like to live in. To use your VA Loan, you must live in the home you wish to buy (no investment properties). Additionally, the property must be eligible for the VA loan. Be sure to pick a realtor that represents buyers to help you with your search. They will tell you if the property is eligible for the VA loan.

Second, you must put an offer in for your home. Most offers require proof of financing eligibility. Remember that talk about credit scores we had earlier? To get proof of financing eligibility, you need to have a good credit score. To learn how to get a good credit score, look HERE.

Third, you will need to put down earnest money and go into an inspection period. Earnest money is proof of interest in the house. A third party holds onto the money and only returns it if you decide to not purchase the home. In some circumstances, if you fail to fulfill your side of the contract, the buyer receives the money and you get nothing in return. If you purchase the home, it goes towards the price You will need to hire a home inspector to ensure there are no major issues with the home. If there are, you can re-negotiate your contract.

Fourth, you will get your home appraised. A special VA appraiser will verify that your home is worth at least as much as the loan the bank is giving you. If it is worth less, you will need to put more money down. The period during inspections and appraisal is called escrow. It starts with your offer being accepted and ends when you close. During this period (which is normally about 40 days) you determine whether or not you’d like to purchase the home based on a number of factors.

Finally, you’ll close on the home. During this time you’ll sign the paper work that gives you the loan for the home and ultimately home ownership. Your monthly payment will usually include some amount of escrow — or monthly payment for things such as taxes and insurance. A few things to consider are below:

Can I afford the monthly mortgage payment?

Don’t forget, this includes monthly insurance and taxes. You still have to pay utilities as well.

How old are key aspects of the home?

Home ownership costs can add up. Items such as HVACs and roofs need to be repaired or replaced about every 15 years.

If there are any other aspects of the home buying process that interest you, please comment below. Our next post will focus on the specifics of the VA loan that make it great.$

10 thoughts on “So You Want to Buy A House? How to Use your VA Loan”