In our last post, we discussed building real estate wealth through appreciation: buying homes with the intent of selling them for more than you purchased them. Today, we will examine two key metrics to look at if you are looking for rental income and later discuss a step by step process to ensuring you are ready to rent your home.

For those of you familiar with the VA Loan, you know that you cannot purchase a home with the intent of renting it immediately (unless it is a duplex and you occupy one side). That being said, you can purchase a home knowing that you will one day rent it. Today, we will discuss two key metrics to look at when home shopping if you intend to rent when you PCS or move out of the home you purchase.

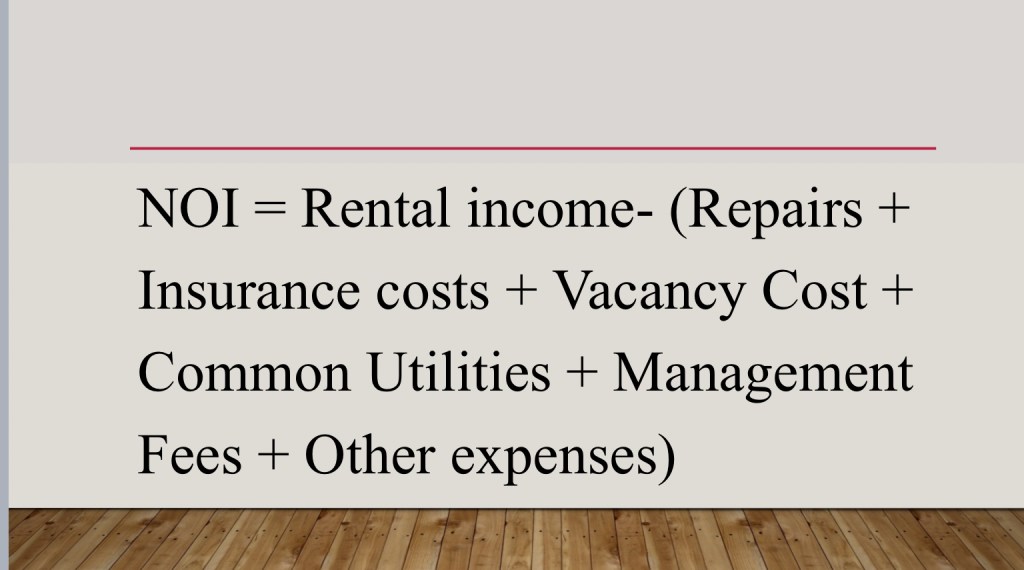

The first metric we will look at is net operating income. Net operating income is defined as the gross rental income you receive minus expenses. Say you make $1,000 a month on a property in rent. However, you spend $50 on insurance, $100 on property management, and average $50 on repairs. The net operating income for that property is $800 per month.

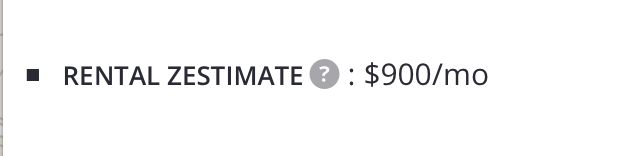

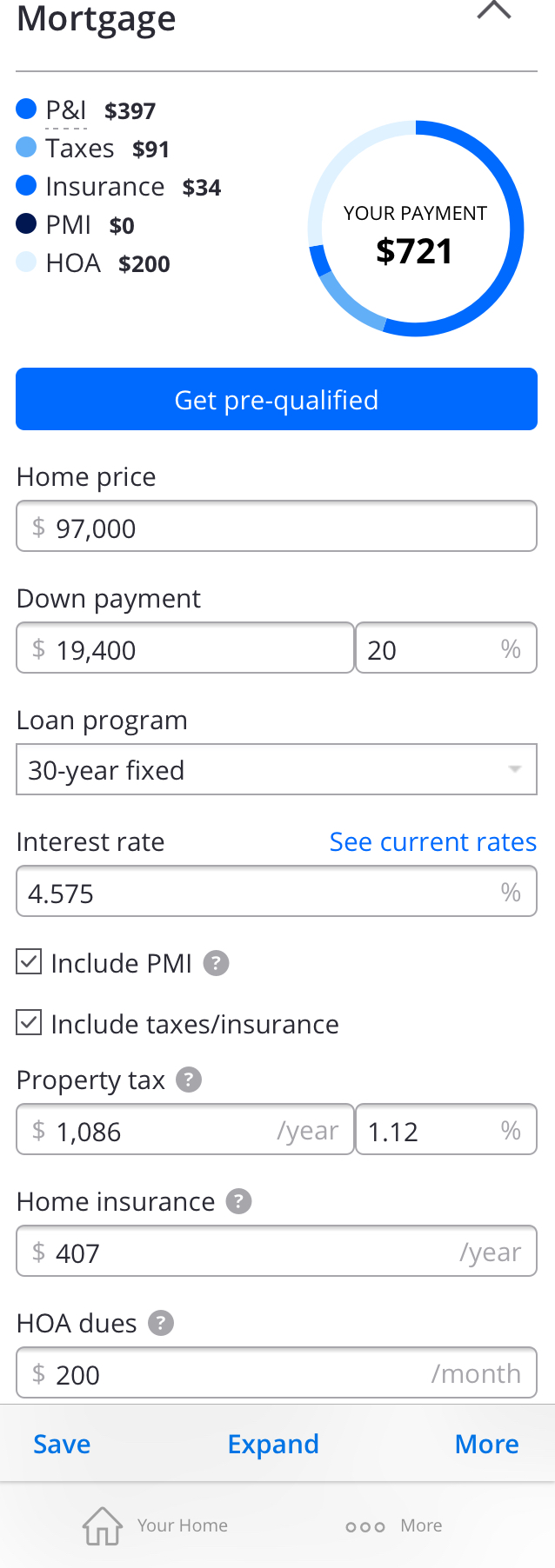

Net operating income changes when you look at the cost of your mortgage. When examining a property you would like to purchase, you must consider your total mortgage cost (to include taxes and insurance) and compare that to your potential rental income. This should give you an idea of what you can expect to make in income each month. Zillow and other tools give you a great way to examine those values. In the pictures below, the home listed rents for an estimated $900 a month and costs you $721 in mortgage and escrow. You might think that means you pocket $179 a month but you must consider property management fees which are typically about 10% as well. Realistically, you’ll net just $89 a month when you have a tenant renting your home.

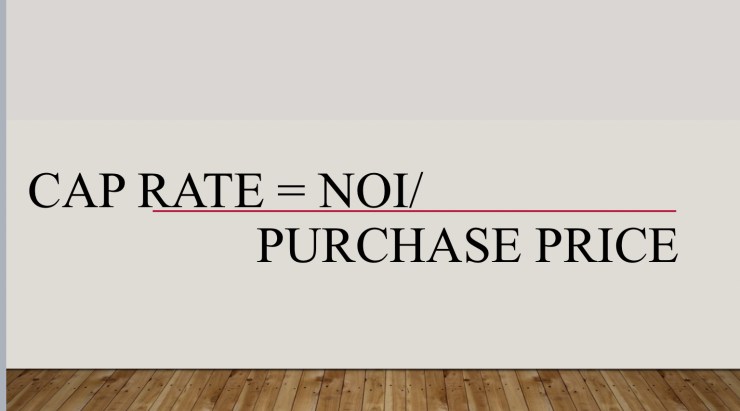

The second metric we will look at is capitalization rate. Generally speaking, cap rate is net operating income divided by purchase price. We won’t go super deep into the calculations (there are very complicated versions) and we’ll make this as easy to understand as possible. If you net $10,000 annually on a home that is $100,000, the cap rate for that home is 10%. This would be an exceptional deal as such a home would “pay for itself” in just 10 years. Your goal should be to find a home with with the best cap rate possible (if you’re looking for rental income), as such a home will provide a good return in terms of rental income.

TLDR: Now that you are familiar with two common rental metrics I’ll discuss two metrics I personally use to screen properties that require minimal calculations.

First: Can you cover a 15 – year mortgage with rental income? If the answer is yes, the property has a better cap rate than most. If you cannot, the home might be too expensive or too nice — there is a diminishing return on rental income based on house size and improvements.

Second: What is the total annual expected rental income divided by the property price? Again this gives you a quick look at what the cap rate is without too many calculations. If it’s greater than 10%, the property is good. If it’s greater than 11% or 12%, that’s really good. $

Enjoy the content of this post? Subscribe below to get the latest content delivered to your inbox!

Looking for additional resources on real estate investing and the VA Loan? Trophy Point Realty’s blog serves as an excellent educational tool and they’re great if you’re PCSing to the Savannah area! https://www.trophypointrealty.com

1 thought on “Real Estate Wealth with the VA Loan: Rentals”