As promised in our previous post , this post will break down the benefits of the VA loan compared to conventional loans. Additionally, we’ll discuss some key facts worth looking at when negotiating a loan. If at any point you’re unsure of what you’re getting into, ask your realtor or loan officer. They should be able to help you through the process.

No Down Payment or PMI

If you’ve ever bought a car before, you may klnow about down payments. In order to have some form of owning interest in a property, most banks require you to foot some of the bill up front. Traditional home loans require a down payment of around 20% or they will charge you an additional fee called PMI. The VA loan does not require any money down and does not charge PMI.

What does this do for you? Say you are trying to finance a $100,000 home. With a conventional loan, you would be required to pay $20,000 up front or pay an additional fee to the bank in case you default. The VA loan waives the $20,000 requirement and does not require you to pay this fee. This allows you to own a home with no money down, which is an opportunity most people do not get.

Attractive Rates and Options

A portion of the VA loan is guaranteed by the government and you are allowed to shop around for financing rather than being required to use a singular source for your loan. What does this mean? It means loan brokers are competing for your business. When people are competing for your business, you get lower rates. Lower rates mean you pay less in interest over time and build equity in your home faster. We’ll talk about what that means later on.

As for options, the VA loan has a few that will help your wallet in the future. First, you have the option to pre-pay at any time. Some loans have pre-payment penalties. What this means is that you are penalized for paying off your loan early. VA loans are not allowed to charge you for paying early so you can pay off your home as quickly as you’d like. Second, you can use your loan for a home, condo, duplex, or newly built home. These options allow you to have choices in where you live. Third, the VA loan is assumable. What this means is that in most cases you can transfer your loan to another VA-eligible individual. If you are having trouble selling your home, for example, you could potentially transfer your loan to another VA-eligible individual. If interest rates are rising, this could help you significantly.

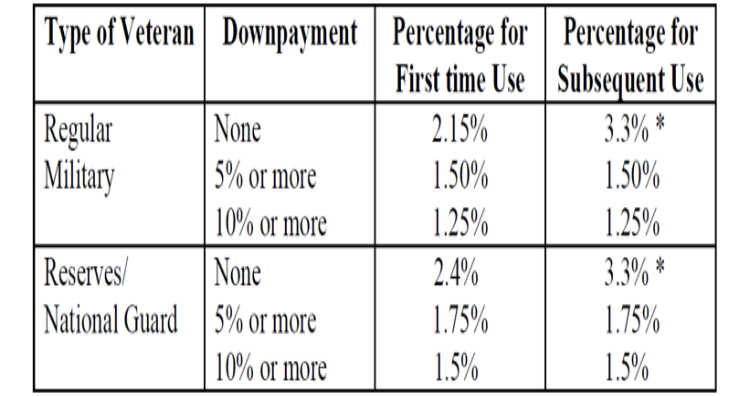

The Funding Fee

The VA loan does require a funding fee that assists with funding future loans. In some cases, wounded veterans and others can have this fee waived. Check with your lender for eligibility. The chart above shows the funding fee required as a percentage of your home price. It is a one time payment that you can pay up front or finance as well. Going back to our previous example, if you purchase a $100,000 home with no money down, your funding fee is $2,150 if this is the first home you’ve purchased using your VA loan.

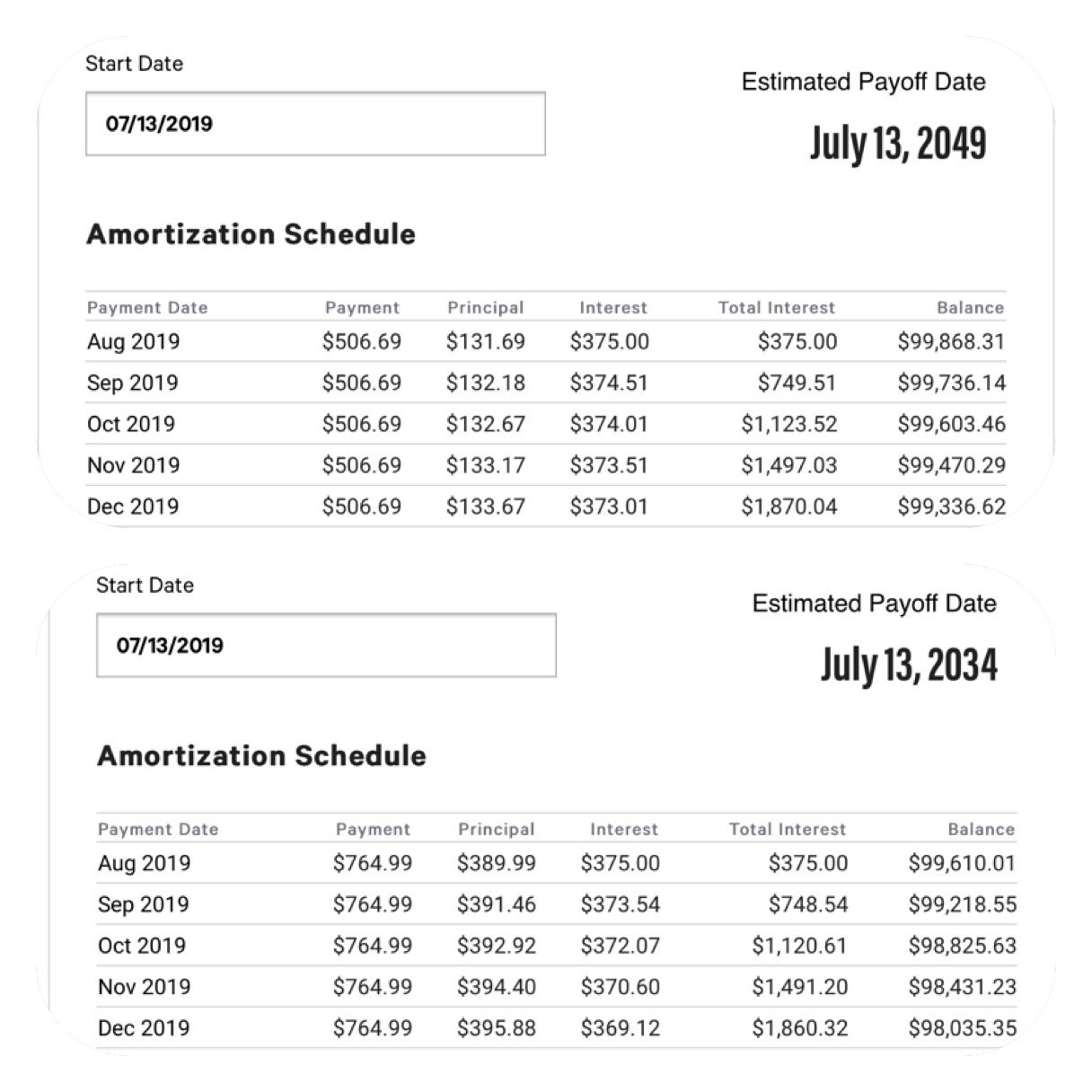

Building Equity and loan options

Sorry for all of the boring tables! However, what’s contained in these tables is worth the look. The table above will help you decide whether to use a 15 or 30 year loan based on how you’re building equity.

Your monthly loan payment is made up of two parts, principal and interest. Principal is money going directly towards the ownership of the house. Interest is money paid to the bank for financing the loan.

Your goal is to build enough principal so you eventually own the home outright. The tables above show a $100,000 loan at 4.5% interest. The top portion shows a 30 year mortgage, the bottom portion shows a 15 year mortgage. Notice the payment is higher on the 15 year mortgage. This is because the loan is spread out over 15 years instead of 30. However, over a 15 year mortgage you pay less interest and you build principal faster. Notice the balance in the far right column decreases much faster for the 15 year loan.

BLUF: If you can afford a 15 year mortgage, you pay off your home faster and you pay less interest.

If you’re interested in running the calculations on your own, click HERE. One area we did not discuss today is adjustable rate mortgages. I highly advise you remain wary of ARMs. Any interest in learning more about ARMs, feel free to send me a note. $

1 thought on “Pros and Cons of the VA Loan (and other home loan facts)”