You’ve probably all heard of it… or at least you were forced to do some online training for the blended retirement system that mentioned it. The Thrift Savings Plan is the primary tool available to government employees, civil servants and the military to invest for retirement. With the new BRS in place for the military and the advent of contribution matches, it is probably worth taking a look at the information available at TSP.gov. But if you’re too lazy to do that, this post will provide a quick overview. Our last post talked about the importance of the snowball effect and how important it is to start investing early… so you should contribute. TODAY! We’ll save alternative investment options for another day.

The TSP enables federal employees to automatically invest up to $19,000 (more in some cases if you’re over 50) a year into one of six funds. Why is this so beneficial? Because it protects your retirement money from taxes. Say you invest your money in a normal account and you make $1,000. Depending on your tax rate and type of retirement account you choose, you may only see $800 of that money you just made. With the TSP you won’t be taxed on your returns if you don’t use them until you retire. You can chose one of two options: Roth and Traditional.

A Traditional TSP takes the percentage of your paycheck you choose before taxes and invests it. You are, in this case, taxed on your returns. In a Roth TSP the percentage of your paycheck you choose to invest is taxed, and your returns on investment are not. Generally speaking you are taxed the same amount, but if you think taxes will go up in the future you should choose the Roth option. Personally, that is what I use.

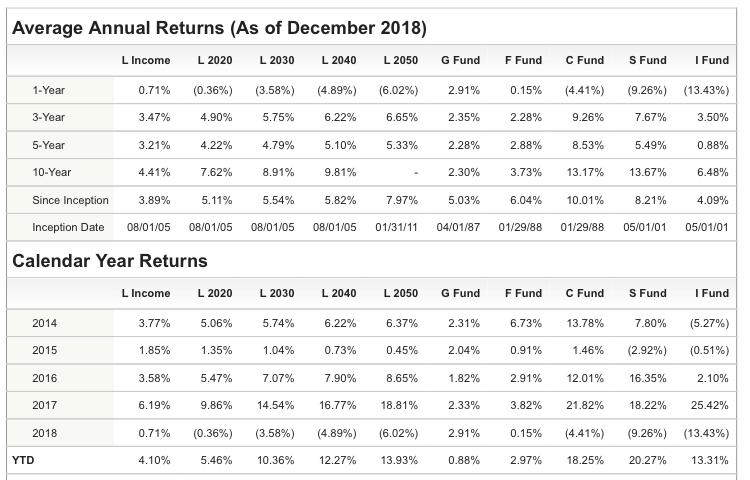

Your fund options are six-fold. You can choose your allocation when you log in at the TSP’s web site. Each fund takes a very small management fee (we’ll talk about indexing and management fees in later posts). I’ll give a brief summary of each fund but first take a look at historical returns in the chart above. As you can see, the C-fund has the highest return since inception and the L-income has the lowest. Each fund is designed for people who believe certain sectors will do well or have a different risk tolerance.

If you’re young, you won’t need your retirement money for a while so you probably have a higher risk tolerance. If you’re closer to 60 (or retirement age) you have a lower risk tolerance as you’ll need your retirement money shortly. The L-funds are designed to automatically make these adjustments as you age. If you’re just starting off investing, I’d recommend the L-funds…particularly the one that reflects when you think you’ll be retiring (i.e. 2020, 2030, 2040 or 2050).

The G-Fund is US treasury securities designed to beat inflation and not lose money. The G-Fund will not necessarily yield a high return but will not lose money. If you are risk averse, the G-Fund is a solid option.

The F-Fund is based on bond prices. It is also low risk but returns begin to decline if companies default on their bonds or inflation increases. If you are somewhat risk averse and have faith in the bond market, this may be the fund for you.

The C-Fund is a direct reflection of the S&P 500 stock index and includes S&P500 dividends. As you can see it has the highest return of the funds listed but it comes with a risk. In the event of a stock market crash, it will likely fall the most of any of the funds available. If your investing horizon is long (i.e. you’re in your 20s) it may be the best fund for you.

The S-Fund is somewhat similar to the C-Fund but mimics the Dow-Jones US Completion total stock market index. It, too is meant for those with long term investing horizons.

Lastly, the I-Fund matches international stock indexes from Europe, Australia, and the far east. If you want to bet on international markets, it’s your best bet.

So why does any of this matter? As an active duty service member or civil servant you have access to an extremely large tax shelter for retirement investment income… $19,000 each year! Most people only have access to their Roth-IRA which is just $5,500 each year. Do yourself a favor and sign up for your TSP today! Otherwise, you’re leaving hard-earned benefits on the table.