In our last post we discussed the TSP and investing options available for those in the military and other employees of the federal government. There is a whole world of investing opportunity outside of the TSP available to the general public as well. This will be the first part of a three part series of posts about investing opportunities other than the TSP. Today’s post will focus on the Roth IRA, expense ratios, and index funds. Feel free to comment if you’re interested in an option that we don’t cover in the series.

The Roth IRA

In our last post we discussed the TSP and the fact that you can contribute $19,000 annually to your TSP account (more if you’re over 50). Depending on the type of account you choose, you’re either not taxed on what you put into your account or you’re not taxed on the returns on that investment. An additional option outside of that account is your Roth IRA. Similar to the Roth TSP option, you are not taxed on investment returns from that account if you don’t make a withdrawal until retirement.

The Roth IRA allows you to invest up to $6,000 a year (2019 limits) into any of a number of Roth-eligible accounts. Your options are much wider than that of the TSP and you have until April 15 of 2020 to contribute for 2019 (The 2018 limit was $5,500 and the deadline was April 15 of 2018). You essentially have 15 and a half months to contribute each year and you can invest in stocks, bonds, index funds, peer to peer lending accounts, and much more. Unlike the TSP, which essentially limits you to one of six funds, the Roth IRA gives you options. If you think that Microsoft stock is the new hotness, you can buy as many shares of MSFT as you can afford in your account… but we’ll talk stocks next time.

Remember the chart we talked about in the snowball post. Think about what happens if you max out your TSP and invest it well in your 20’s. That’s a lot of money. I highly recommend you maximize your contribution every year.

What’s an Expense Ratio?

Have you ever sold all of the shares of your mutual fund or index fund and wondered why you didn’t get all of the money in your account? I remember the first time I did that and I was shocked. That’s because if you invest outside of the TSP (the TSP does take a small expense ratio) you are generally charged a small management fee when you sell. These fees can range from around 0.10% to around 2.5% depending on a number of factors and are called expense ratios.

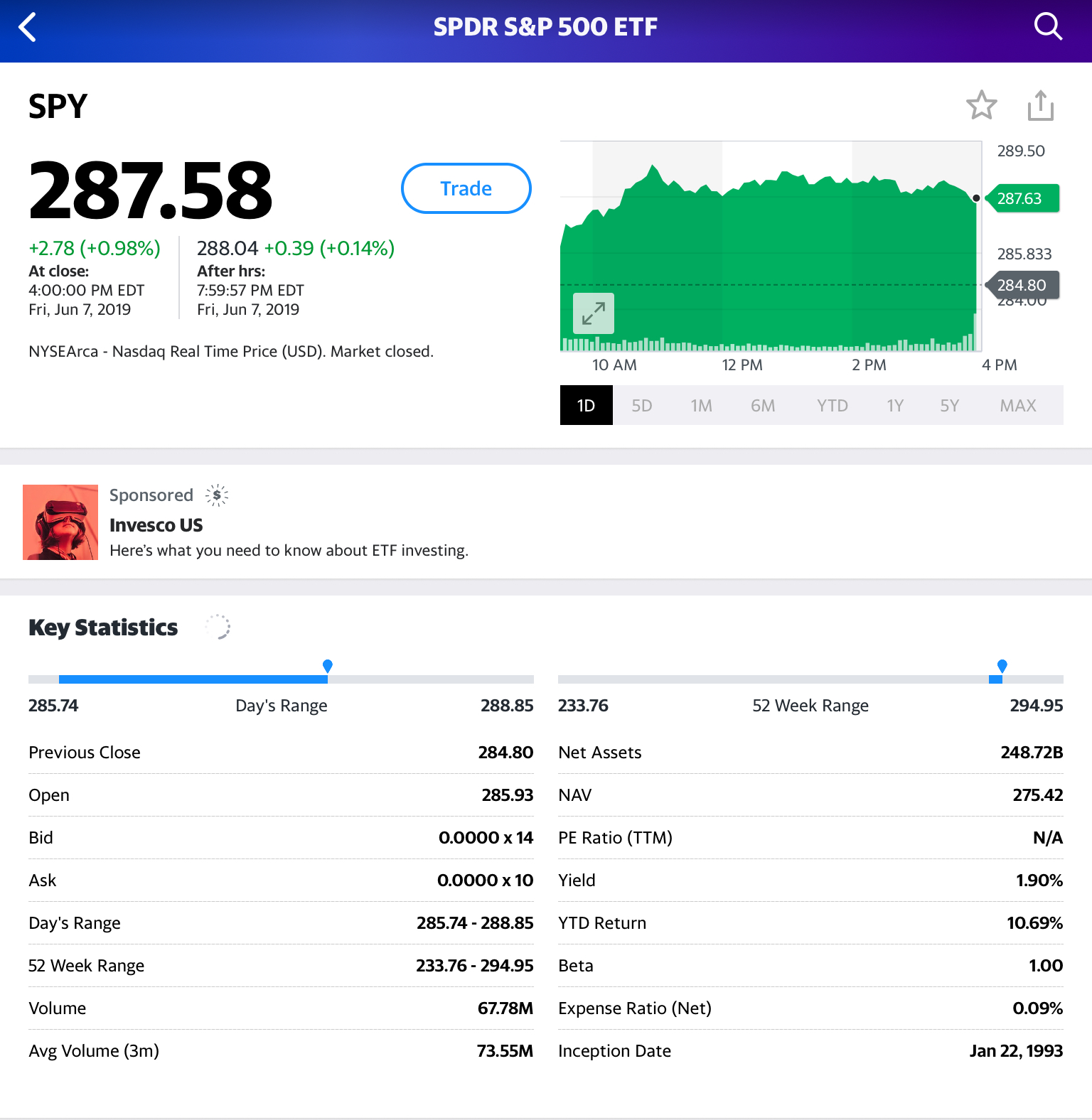

Take a look at the snapshot of SPY, the S&P500 ETF from Yahoo finance above. You can see the expense ratio is 0.09%. If you sold $10,000 of SPY today, you’d have an account balance of $9,991 with the 0.09% or $9 taken out. With some actively managed funds, the expense ratio gets higher. Again, some are as high as 2.5%. Before you buy any financial product just be sure to check the expense ratio (and other fees) so you know what your fees are when you sell. Two percent may not seem like much but over time it cuts deep into your returns.

As a rule of thumb, actively managed funds generally charge higher expense ratios than passively managed funds. Take a look at the fund background to see what you are buying. I generally recommend index funds given historical returns and lack of management fees. If you’re interested in the difference, read A Random Walk Down Wall Street by Princeton economist Burton Malkiel. That’s a discussion for another day.

Index Funds

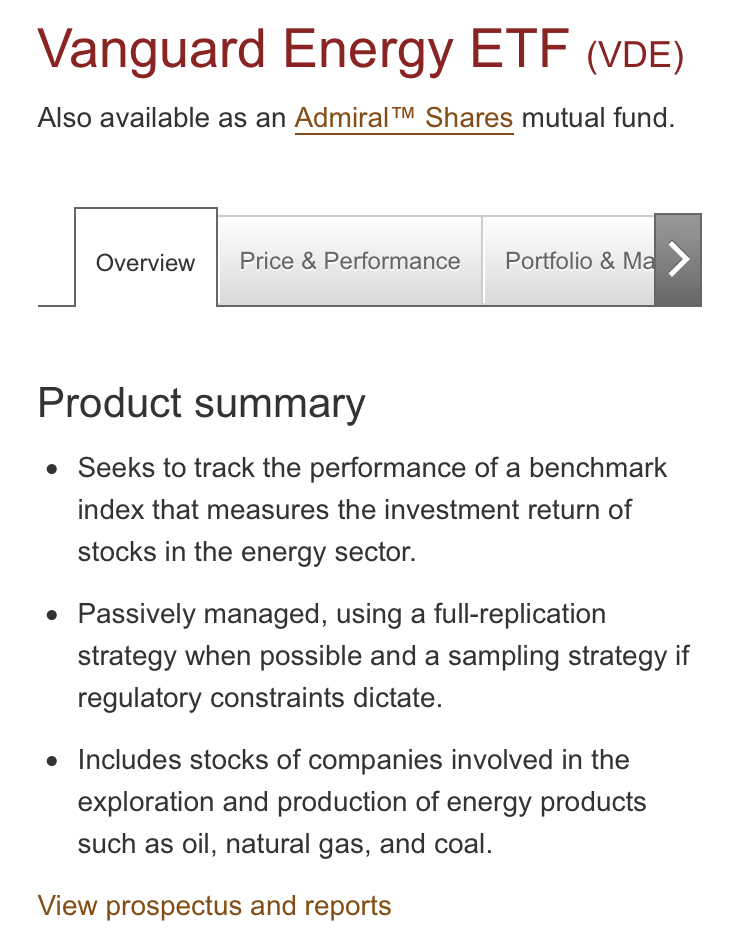

Index funds are one way to invest in the broader stock market with low expense ratios and returns that mimic the market. With index funds, however, you can choose the sector you’d like to invest in. Companies like Vanguard investment group offer a number of funds with low expense ratios. If you’d like to invest in a specific sector, say energy, for example, you can purchase the ETF with ticker VDE. ETFs are index funds that trade like stocks so they are more liquid. This means they can be bought and sold with relative ease. The picture below shows the mobile product description of VDE. Note that the fund invests in a variety of stocks and is passively managed.

The fact that the fund invests in a number of stocks limits your risk of one company failing and you losing all of your money. Passive management means that the fund isn’t buying and selling holdings on a regular basis. With an expense ratio of just 0.10%, this fund is right for you if you’d like to invest in energy. Trading index funds is a worthwhile option if you’re interested in investing outside of the TSP.

If you’re looking to invest for retirement outside of the TSP, avoid taxes on your returns, and pay limited fees, I recommend you contribute to your Roth IRA (maximize it if possible) and invest in index funds or ETFs. Most of the information you’re looking for is just a click away on Yahoo finance.

I appreciate your time today and please share this post with your family, friends, and anyone looking to understand investment options. Stay tuned for the next posts in the series!$