Today’s post really digs into some of the finer aspects of TSP investing. Written by Cinthia Wilkinson (a member of the Air National Guard) of AAFMAA Wealth management and trust, it focuses on risk tolerance and the decision to invest in a Roth vs traditional TSP.

The Thrift Savings Plan (TSP) is a defined contribution retirement plan — like a 401(k) — for members of the military and federal employees.

As an investor in the TSP, you choose how much you’d like to invest, and then have options on how to manage that money, including five individual index funds, or lifecycle funds (called an “L Fund”).

You can get a detailed overview about the funds and their performance using TSPs Fund Information Sheet, or more abbreviated information on their Fund Information Card.

If you are new to investing, you may try different asset allocation calculators via Google search to assist you in determining how to apportion your money, or speak with a Relationship Manager at AAFMAA Wealth Management & Trust (AWM&T) for a more tailored recommendation.

It’s important to know whether you are in the Blended Retirement System or High 3-Year (High-36 month) legacy system. The BRS system provides up to 5% matching from your government organization whereas the legacy system does not include matching.

The IRS limits how much money any individual can save toward retirement per year; with good financial planning, you can maximize your annual contributions.

For 2020, the max limit is $19,500 toward 401(k), 403(b), TSP and 457 plans. You can

contribute up to $6,000 toward a Traditional or Roth IRA account, assuming you are

within the allowable income limits* and below the age of 50*. If you are older than 50, you can contribute an additional $1,000 into the IRAs known as catch-up contributions.

Actively employed TSP participants age 50 and older can also make TSP catch-up

contributions of an amount ($6,500 in 2020) above the elective deferral limit amount

($19,500 in 2020).

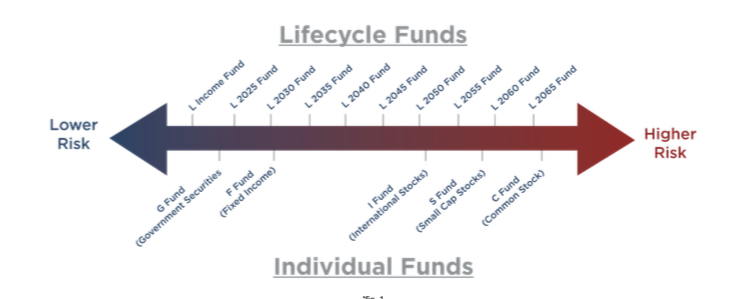

Lifecycle Funds vs. Individual Funds

In the same way that the TSP is similar to a 401(k) or IRA, the Individual Funds and Lifecycle are the same as the mutual funds and target retirement funds that civilians purchase.

Individual funds allow you to invest in five index funds, focused on everything from short-term U.S. Treasury security to domestic and international stocks. Each index fund has its own risk category, and you can rebalance your investments depending on your tolerance and circumstances. The G (Government Securities Investment) Fund is like a money market fund and the F (Fixed Income) Fund invests in bonds issued by U.S. companies.

You also have the opportunity to invest in a variety of global stocks: the C (Common Stock) Fund, large, well-known U.S.-based companies, S (Small Cap Stock), small-to-mid-sized U.S. companies, and I (International Stock) Funds, non-U.S. companies.

Lifecycle funds use a diversified mix of the five core individual index funds and are based on the year you will need your money. These funds are automatically rebalanced every quarter by adjusting the percentage of stocks and bonds, shifting more to bonds as they get closer to their target dates.

For example: If you are invested in the L 2065 Fund, more of your money will be in

the C, S and I Funds than in the G and F Funds. If you have purchased the L 2025

Fund, the majority of your money will be invested in the G and F Fund than in the C, S, and I Funds.

*It’s important to note that only two interfund transfers are allowed per month in the

TSP; any subsequent transfers can only be added to the G Fund.

Risk Tolerance

When selecting TSP investment options, it’s important to consider your risk

tolerance: your ability to emotionally and financially endure the possibility of losing money on an investment, even if there is a potential for long-term gain.

If your risk tolerance is low, regardless of the potential for gain, you may be

uncomfortable with fluctuations in your retirement accounts. The opposite is true for investors who have a higher risk tolerance. Financial goals, timeline, and age are all factors that can determine individual risk tolerance.

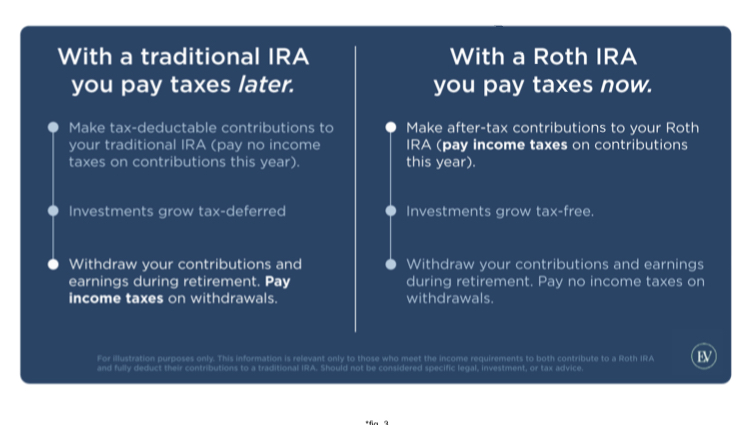

ROTH vs. Traditional IRA

Both Roth and traditional IRAs are important investment tools for retirement that provide tax advantages while you save. Each has its own eligibility, contribution and withdrawal guidelines, so be sure to connect with your AWM&T Relationship Manager for information and recommendations.

Roth IRAs can be helpful if you anticipate you’ll be in a higher tax bracket when you retire. Because the money invested in a Roth IRA has already been taxed, your qualified withdrawals are tax-free. Traditional IRAs allow you to reduce your current tax burden by investing in retirement savings, however the money will be taxed when it’s time to

withdraw it.

How do you determine which IRA is right for you? There are a number of circumstance that can impact this investment decision, but a common one is your future tax bracket: If you think your tax bracket will be higher at a future date, consider a Roth IRA account; if you think that your tax bracket will be lower in the future, a traditional IRA might be a better fit.

Examples:

You are an E-3 with four years of service currently and plan to retire as an E-8 with 24 years of service without a secondary career: Consider a traditional IRA.

You are an E-8 with 20 years of service, retiring from the service and taking on a GS-14 position as a second career: A Roth IRA might be a better option.

*If you decide to invest in a Roth or traditional IRA, it’s important to consult with your tax professional.

We hope you enjoyed the content of this post! Subscribe below to get the latest content delivered to your inbox!

Great stuff, as always.

LikeLiked by 1 person